As AMD announces that their Q1 revenue will fall significantly short of expectations, the biggest question that poses itself is why things are so much worse than in Q4, but also how difficult it will be to fix, and what other profitability numbers should be expected in Q1 and Q2 2007 for both CPUs and GPUs. Read on to see what we think, and what industry dynamics are at play...

A quick look at the numbers

The press release issued by AMD indicated that revenue would be down to $1.225B, from previous company forecasts of $1.6-1.7B. That original forecast was only 5% lower than Q4's revenue, so it might look like AMD was only expecting a seasonal decline; but there's a catch. The results for Q4 only included ATI's results as of October 25, and thus were probably about $150M lower than they would have been with a full quarter of ATI sales.

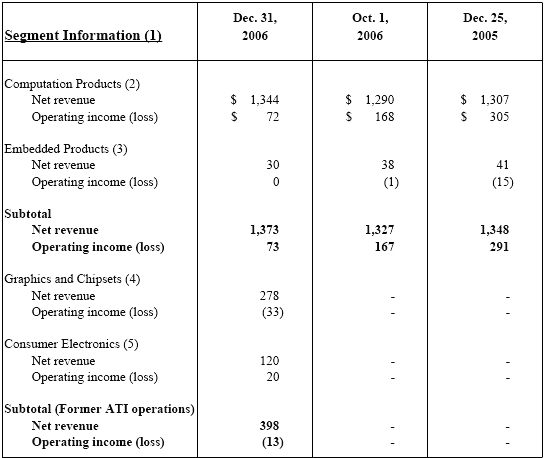

So, still nothing drastic, but it's worth pointing out that this implies that the analysts' revenue expectations went down three times already for this quarter and that, compared to what was expected in December, it's probably at least 35% down. So, what part or parts of the business were most affected? Let's look at AMD's official figures for Q4 2006 first. Here are most of the interesting numbers, excluding the balance sheet and operating expenses:

Based on this, we can first conclude that there is nearly $500M of revenue "missing" compared to Q406, even after taking seasonality into consideration. Indeed, including a full quarter of ATI operations, Q406 should have been in the $1.9B+ range so Q107 should have been around $1.8B! Furthermore, let's look at the exact statement AMD made in their press release yesterday:

Revenues declined sharply quarter-over-quarter for the Computing Solutions segment, primarily due to lower overall average selling prices and significantly lower unit sales, especially in the resale channel.

Considering the emphasis on Computing Solutions being responsible for the decline, it is quite likely that other business units did not suffer such heavy revenue losses. In the worst case, the entire amount of missing revenue might be attributed to a decline in Computing Solutions, which would then decline to as little as $800M. That would represent a 40% quarter-over-quarter decline, which is not strictly impossible but obviously fairly dramatic. In the best case, financially speaking, only $250-300M of the missing revenue may be attributed to a decline in Computing Solutions, with the former-ATI revenue declining also quite sharply.

The reason why we say that a decline in former-ATI revenues would be financially positive is that the CPU business, even after all the ASP declines, still likely has slightly higher gross margins than chipsets or GPUs. However, ATI had vastly different margins in Graphics, Chipsets and Consumer Electronics; as such, obviously, a decline in Consumer Electronics would be even worse, while one in Chipsets would be much less dramatic because that represents significantly less gross profit. In terms of CPUs, it should also be considered where AMD most likely suffered the most; in servers or in clients (aka desktops/laptops)? Once again, the former has higher margins than the latter.

Since we now realise what could have happened, let's look at what dynamics are occuring in AMD's different business units and try to determine the most likely scenarios of what happened in Q1 2007.